Financial Literacy

Middle-aged borrowers are defaulting at record rates, and the damage to household finances now spans decades.

What to Know

- 2.6 million borrowers defaulted on student loans in Q1 2026 alone

- Average student loan defaulter is now nearly 40 years old

- 8.8 million borrowers are currently in default or severe delinquency

- 26% of all outstanding student debt is held by borrowers age 50 and older

- Retirement balances for workers over 50 with student debt are 30% lower than peers without it

America's student debt crisis has aged. It is no longer a story about recent graduates struggling through entry-level years. It is now a story about workers in their late thirties and forties, with mortgages, children, and retirement deadlines, falling behind on loans they took out decades ago.

Wall Street Journal reporting on New York Federal Reserve data confirms the shift. CNBC and Federal Reserve analysis show 2.6 million borrowers entered default in just the first quarter of 2026, and the average defaulter is nearly a decade older than the image most Americans carry of who student debt actually hurts.

Default Is No Longer a Young Person's Problem

Student loan delinquency hit 10.3% in Q1 2026, with $92.6 billion in balances sitting between 271 and 360 days past due as of late 2025. Borrowers are not defaulting because they never earned degrees. Many earned them, built careers, and still could not outpace interest accumulation on balances that grew during deferment, forbearance, and pandemic pauses.

26% of all outstanding student debt is now held by Americans 50 and older. Borrowers who took out loans for graduate school, career changes, or to support children through college are carrying balances well into what should be their peak wealth-building years.

Homeownership and Retirement Are Paying the Price

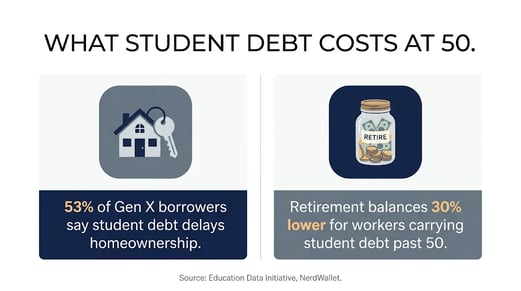

Debt does not just delay milestones. It permanently reprices them for millions of households across the country. 53% of Gen X borrowers say student debt is directly delaying homeownership, meaning households that cannot build equity are also missing the primary wealth-accumulation vehicle available to middle-class Americans.

Student debt shrinking retirement savings for older American workers. Created via Gemini.

Retirement is taking a harder hit. Workers over 50 carrying student debt hold retirement balances 30% lower on average than peers without it. At that stage in a career, a 30% gap in savings does not close, leaving borrowers more dependent on Social Security and less able to absorb health costs or job disruptions in their final working years.

Broken Pipeline, Not Bad Borrowers

Millions of middle-aged defaulters followed every rule they were given. They borrowed within federal limits, attended accredited institutions, and entered repayment on schedule as instructed.

-png-3.png?width=280&height=241&name=image%20(2)-png-3.png)

Natalia Abrams, President, Student Debt Crisis Center

Abrams, speaking to NPR on rising defaults, stated:

"These are not irresponsible people. These are people who did everything right and the system failed them."

What changed was the cost structure of American higher education, which grew faster than wages for three consecutive decades, and a repayment system never designed to handle balances this large on incomes this flat. Calling this an individual failure obscures what is fundamentally a structural one.

Wrap Up

A financial system that regularly produces 40-year-old defaulters is not functioning as designed. Higher education was sold to American households as the clearest path to middle-class stability. For millions of borrowers, it has become the primary obstacle to it.

Policymakers can extend timelines, adjust payment formulas, and offer targeted relief. But none of those tools address why balances grew this large or why wages failed to keep pace, and until those questions are answered honestly, the average age of a defaulter will keep rising. Ordinary Americans deserve a financing model for education that does not ask them to choose between their student loans and their retirement.